I want to start by saying this is NOT GOOD FOR AMD.

http://www.digitimes.com/systems/a20061024PR211.html (this link now needs a log in)

http://dailytech.com/article.aspx?newsid=4706

If you look at my posts/comments over the last few days I have been saying Dell is dragging AMD down the price stack and squeezing them on pricing thus hurting margins. I am now convinced this is what is happening. I know I said yesterday that AMD needs to do some discounting on notebooks to gain entry into new customers to break Intel's stronghold in the notebook segment but this sounds like they are going to start hurting themselves.

I repeat, if AMD was not running tight on capacity then it's ok to do these kinds of deals to keep the factories loaded. But considering the reports that they are starving teh channel on desktop parts for the last few months and now the TW ODMs are saying AMD may be short of mobile parts, surely they could have made some of these a higher bin and sold them for better margins at some of the other customers they are gaining entry into. Dell has no strategy and is heading into a death spiral of becoming commoditized but it's tragic they are dragging AMD down. As much as I think Intel is going to gain the momentum for the next 6-9 months, I think AMD is now throwing away the strategic leverage they have built so successfully in the market place with a good range of customers through these deals with Dell.

UPDATE

Dell's new AMD based notebooks are not sub 500$. In fact, a quick spec comparision shows they may actually be more expensive than an equivalent Centrino Duo. We probably need to wait 1-2 quarters to really see how this plays out.

Thursday, October 26, 2006

Wednesday, October 25, 2006

This is kind of funny

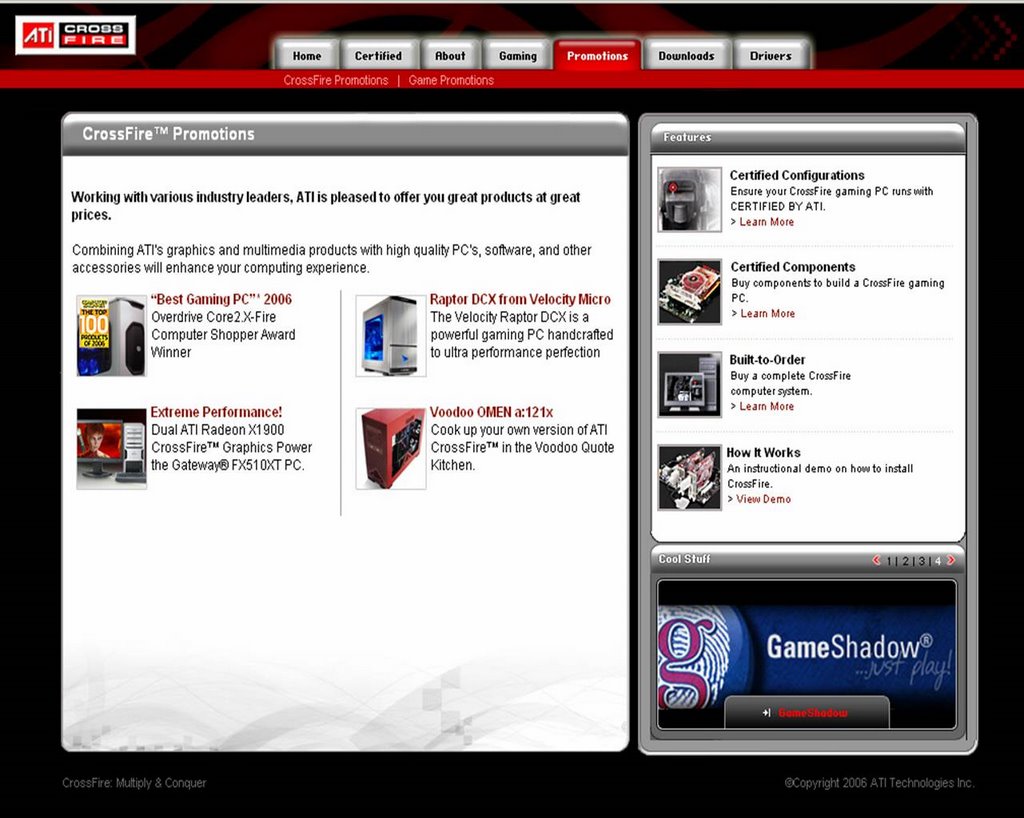

AMD which has just acquired ATI is promoting Crossfire systems with 3 out of 4 being Core 2 systems as best in class for gaming. I screen grabbed them before they get removed...

What makes this really funny is this is not on the ATI site but on the AMD site:

http://ati.amd.com/technology/crossfire/promotions.html

I wonder how quickly this comes down? Someone is getting a flamer in their e-mail when they get into work tomorrow!

What makes this really funny is this is not on the ATI site but on the AMD site:

http://ati.amd.com/technology/crossfire/promotions.html

I wonder how quickly this comes down? Someone is getting a flamer in their e-mail when they get into work tomorrow!

AMD Earnings - a quick note

I want to move past the earnings announcements quickly cos they're stale news and I've taken too long to get to this. Hence, just a quick note on AMD:

1. Overall, their quarter came in on track more or less as I'd predicted including the fact they'd have a better quarter of it than Intel financially. The market share discussion also sees some light with the following assessment from Mercury Research - that both gained share from Via but Intel gained 3 points of share while AMD gained 1 point. The key here is AMD's leaps in market share are abating.

Q3 06 Market Share

2. The inventory issue (up by 15%) is worrying and my assessment is that this build up is really a result of Dell not being able to sell everything that was built for them...or just having the wrong SKUs.

3. Margins took a substantial beating down ~5.5%. A few things happened here. First, AMD's growth in servers slowed down relative to the pace they've been managing past few quarters due to Woodcrest. Those margins were allowing them to sell client parts (desktop specifically) at a large discount to gain share. Second, Intel competitive pricing really hit them and they had to take big price drops in the desktop segment which is where they have strength after server. Third, they are chasing low margin deals like Dell to secure entry into new customers like Dell and the PRC OEMs.

4. Unit volume growth was high but overall market share gain was just 1%. Intel took 3% - all of it from Via. I'd also predicted that they would do everything to keep their factories full and it looks like they did.

5. They are clearly short-changing the channel on supply and price competitiveness and this is a chink in their armour that will hurt them over the next few quarters.

Looking forward, AMD didn't provide much in the way of guidance. My thoughts:

- It is crucial for them to win back Opeteron share where they are losing to Woodcrest. I suspect they think Dell will help them do that but you cannot have Woodcrest grow to 40% of the DP market by unit and assume it's all the low end of the market from a system pricing POV.

- They should hold desktop pricing even if it means losing share and hope pricing stabilizes as Intel & AMD have said it might.

- Mobile - they should be willing to drop price in this segment to gain entry into new customers before Intel launches Santa Rosa. Frankly, even though AMD claims a 50% sequantial growth in mobile QoQ, considering the small base they have this is probably not as impressive as it sounds when you think the mobile market is growing at 20-30%. If they hope to dent Intel's stranglehold on this high margin segment they must be willing to make some trade offs.

Overall, looking into Q4 I think AMD still has it's job cut out. They will reap the benefits on cost and hence margins moving to 65nm but will be negated by their need to sustain market share. I would not be surprised if Intel extended it's Oct 22 price drop beyond low end desktop SKUs if required to keep AMD on the defensive. They need to gain market share because adjusting inventory to customer needs is easier said than done so that optimization they talk about may or may not happen. The incremental 60 million worth inventory accumulated this qtr if they've built the wrong product is going to either have to be sold or written off. Either way, it's going to hurt. Operating cash is important because they now have an ATI acquisition to pay debt on. AMD has a dilemma pulling them in two opposite directions. I suspect in Q4 they will actually cede share to hold pricing and margins. While everyone is focussed on AMD starting 65nm shipments, Intel too is increasing their 65nm and reducing 90nm every day so the battle for cost efficiency is tough...specially since the Core products have smaller die sizes.

With nothing left of Via, next quarter will truly tell who is gaining share and who is losing it. I still predict AMD will lose share and Intel will gain it. Remember, 3% of the remaining market is more than 1% in absolute volume terms. Momentum is swinging back to Intel and Q4 will show us that.

1. Overall, their quarter came in on track more or less as I'd predicted including the fact they'd have a better quarter of it than Intel financially. The market share discussion also sees some light with the following assessment from Mercury Research - that both gained share from Via but Intel gained 3 points of share while AMD gained 1 point. The key here is AMD's leaps in market share are abating.

Q3 06 Market Share

2. The inventory issue (up by 15%) is worrying and my assessment is that this build up is really a result of Dell not being able to sell everything that was built for them...or just having the wrong SKUs.

3. Margins took a substantial beating down ~5.5%. A few things happened here. First, AMD's growth in servers slowed down relative to the pace they've been managing past few quarters due to Woodcrest. Those margins were allowing them to sell client parts (desktop specifically) at a large discount to gain share. Second, Intel competitive pricing really hit them and they had to take big price drops in the desktop segment which is where they have strength after server. Third, they are chasing low margin deals like Dell to secure entry into new customers like Dell and the PRC OEMs.

4. Unit volume growth was high but overall market share gain was just 1%. Intel took 3% - all of it from Via. I'd also predicted that they would do everything to keep their factories full and it looks like they did.

5. They are clearly short-changing the channel on supply and price competitiveness and this is a chink in their armour that will hurt them over the next few quarters.

Looking forward, AMD didn't provide much in the way of guidance. My thoughts:

- It is crucial for them to win back Opeteron share where they are losing to Woodcrest. I suspect they think Dell will help them do that but you cannot have Woodcrest grow to 40% of the DP market by unit and assume it's all the low end of the market from a system pricing POV.

- They should hold desktop pricing even if it means losing share and hope pricing stabilizes as Intel & AMD have said it might.

- Mobile - they should be willing to drop price in this segment to gain entry into new customers before Intel launches Santa Rosa. Frankly, even though AMD claims a 50% sequantial growth in mobile QoQ, considering the small base they have this is probably not as impressive as it sounds when you think the mobile market is growing at 20-30%. If they hope to dent Intel's stranglehold on this high margin segment they must be willing to make some trade offs.

Overall, looking into Q4 I think AMD still has it's job cut out. They will reap the benefits on cost and hence margins moving to 65nm but will be negated by their need to sustain market share. I would not be surprised if Intel extended it's Oct 22 price drop beyond low end desktop SKUs if required to keep AMD on the defensive. They need to gain market share because adjusting inventory to customer needs is easier said than done so that optimization they talk about may or may not happen. The incremental 60 million worth inventory accumulated this qtr if they've built the wrong product is going to either have to be sold or written off. Either way, it's going to hurt. Operating cash is important because they now have an ATI acquisition to pay debt on. AMD has a dilemma pulling them in two opposite directions. I suspect in Q4 they will actually cede share to hold pricing and margins. While everyone is focussed on AMD starting 65nm shipments, Intel too is increasing their 65nm and reducing 90nm every day so the battle for cost efficiency is tough...specially since the Core products have smaller die sizes.

With nothing left of Via, next quarter will truly tell who is gaining share and who is losing it. I still predict AMD will lose share and Intel will gain it. Remember, 3% of the remaining market is more than 1% in absolute volume terms. Momentum is swinging back to Intel and Q4 will show us that.

Monday, October 23, 2006

Comparision points

Folks - I'm in the process of my analysis on the Q3 earnings but stopped to make a point on how everyone is using YOY (year on year) or QOQ (qtr on qtr) results selectively. They both serve different purposes and with some astute (non-biased) interpretation can be used together to give you a good read. However, don't ignore the changes in the marketplace:

1. AMD will start using 65nm which will give them cost and capacity boosts.

2. Core 2 has smaller die sizes than Netburst...and even some of AMD's line up.

3. Intel has a brand new top-to-bottom product line that kicks ass. AMD does not have a response till mid 2007.

4. AMD has a huge new customer - Dell. But Dell is losing share and more importantly their strategic direction.

5. Intel also has a new customer - Apple. Who is growing their own PC client columes at a fast clip. But is probably getting mobile parts significantly cheaper than anyone else from Intel.

6. AMD has a new strategic acquisition - ATI. But it is unlikely we will see a corporate platform from them in 2007. But they will now have the ability to make life very difficult for Intel in the short term on the integrated graphics business through bundling and pricing. Also, ATI has a strong brand...I'd venture to say perhaps even stronger than AMD in the high end consumer space.

Bottom-line, there isn't a deciding factor to who wins. Some well rounded analysis will engender some good discussion. A single data point (i.e. gross margin) doesn't mean victory for one side or the other (in this case I mean the pro Intel/AMD folks).

I'll be back shortly with my look at the Intel earnings.

1. AMD will start using 65nm which will give them cost and capacity boosts.

2. Core 2 has smaller die sizes than Netburst...and even some of AMD's line up.

3. Intel has a brand new top-to-bottom product line that kicks ass. AMD does not have a response till mid 2007.

4. AMD has a huge new customer - Dell. But Dell is losing share and more importantly their strategic direction.

5. Intel also has a new customer - Apple. Who is growing their own PC client columes at a fast clip. But is probably getting mobile parts significantly cheaper than anyone else from Intel.

6. AMD has a new strategic acquisition - ATI. But it is unlikely we will see a corporate platform from them in 2007. But they will now have the ability to make life very difficult for Intel in the short term on the integrated graphics business through bundling and pricing. Also, ATI has a strong brand...I'd venture to say perhaps even stronger than AMD in the high end consumer space.

Bottom-line, there isn't a deciding factor to who wins. Some well rounded analysis will engender some good discussion. A single data point (i.e. gross margin) doesn't mean victory for one side or the other (in this case I mean the pro Intel/AMD folks).

I'll be back shortly with my look at the Intel earnings.

Sunday, October 22, 2006

Intel Q3 06 earnings analysis

Been busy this weekend and just able to grab a little time to listen to the earnings properly:

1. Server revenue, double digit unit growth and ASP growth - this is a very healthy sign. As I had said earlier, Intel is starting to win back their big losses in servers...specially in the DP space. Combine that with the fact that Woodcrest is already 40% of the server market by volume in 3 months (as announced at IDF first). However, the impact of this may be felt less to AMD if they decide to retain premium pricing on Opteron and really focus on the MP server market where margins are higher.

2. Mobile too had record shipments - at the cost of desktops which continue do decline as a share of overall market. Not unexpected as Intel does have a significant lead over AMD in mobile. Will be interesting to see the impact of Dell in this space in Q4. But with Merom ramping incredibly fast considering it would be the bulk of the volume in the Core 2 6 million units shipped, feels like they're in good shape here.

3. Inventory in microprocessors down QoQ. Chipsets and flash were up. Overall inventory was ~4.45 billion...a gain of 120 million over Q2. They also took a 100 million $ write off. But most importantly, all the WIP is 65nm. Which means the transition is happening quite rapidly.

4. Q4 outlook - revenue between 9.1 to 9.7 billion. Gross margin around 50%. On track to hit 95,000 heads from 102,500. About 500 million savings on capital spending and R&D against the original plan. MG&A costs to be about flat QoQ even as revenue increases. Overall, it looks like the effects of the re-structure are kicking in to the upside. The worrying thing here is the gross margin staying at 50%. Which means either the price war will continue or they will get hit with the 65nm and 45nm transition costs. Since the indication from Bryant is they expect to see prices firm n Q4, this is probably the former.

On the face of it, the qtr came through pretty much as I expected. Otellini believes they gained overall share but as I said earlier, we'll have to wait for Gartner/IDC to confirm. The most critical piece in here is servers and the Woodcrest ramp. The more share they re-gain here, the harder they hit AMD's margins and hence free cash which is very important as AMD takes incremental debt to fund the ATI acquisition. The price war should stabilize in Q4. Obviously Intel had planned for this when they forecast their margin at 49%. Overall, it feels like Intel is holding in mobile, winning back in servers and losing in desktop. While it's important to win back the desktop market just because of the sheer size, I think we will see the true impact of the price drops and the Core 2 introduction in Q4 due to the lack of lower cost motherboards.

My nett take away is the qtr went as planned. Woodcrest is the bright spot and some marginal upside in terms of revenue but nothing to write home about. A concern on margins for Q4 and the discussion on share still up in the air as Otellini claims they gained overall share and it isn't clear from a quick glance at AMD's call whether they believe they gained any. However, I'll be reviewing that in detail next and will see if we can call it. For now, Intel needs to stay the course and focus on ramping Core 2 desktop, get the right chipsets/boards into the channels and help their OEM customers get off to a quick start as they introduce products this quarter for Christmas.

I'll be reviewing AMD's results next and will be able to figure out what I think Q4 will look like based on that.

1. Server revenue, double digit unit growth and ASP growth - this is a very healthy sign. As I had said earlier, Intel is starting to win back their big losses in servers...specially in the DP space. Combine that with the fact that Woodcrest is already 40% of the server market by volume in 3 months (as announced at IDF first). However, the impact of this may be felt less to AMD if they decide to retain premium pricing on Opteron and really focus on the MP server market where margins are higher.

2. Mobile too had record shipments - at the cost of desktops which continue do decline as a share of overall market. Not unexpected as Intel does have a significant lead over AMD in mobile. Will be interesting to see the impact of Dell in this space in Q4. But with Merom ramping incredibly fast considering it would be the bulk of the volume in the Core 2 6 million units shipped, feels like they're in good shape here.

3. Inventory in microprocessors down QoQ. Chipsets and flash were up. Overall inventory was ~4.45 billion...a gain of 120 million over Q2. They also took a 100 million $ write off. But most importantly, all the WIP is 65nm. Which means the transition is happening quite rapidly.

4. Q4 outlook - revenue between 9.1 to 9.7 billion. Gross margin around 50%. On track to hit 95,000 heads from 102,500. About 500 million savings on capital spending and R&D against the original plan. MG&A costs to be about flat QoQ even as revenue increases. Overall, it looks like the effects of the re-structure are kicking in to the upside. The worrying thing here is the gross margin staying at 50%. Which means either the price war will continue or they will get hit with the 65nm and 45nm transition costs. Since the indication from Bryant is they expect to see prices firm n Q4, this is probably the former.

On the face of it, the qtr came through pretty much as I expected. Otellini believes they gained overall share but as I said earlier, we'll have to wait for Gartner/IDC to confirm. The most critical piece in here is servers and the Woodcrest ramp. The more share they re-gain here, the harder they hit AMD's margins and hence free cash which is very important as AMD takes incremental debt to fund the ATI acquisition. The price war should stabilize in Q4. Obviously Intel had planned for this when they forecast their margin at 49%. Overall, it feels like Intel is holding in mobile, winning back in servers and losing in desktop. While it's important to win back the desktop market just because of the sheer size, I think we will see the true impact of the price drops and the Core 2 introduction in Q4 due to the lack of lower cost motherboards.

My nett take away is the qtr went as planned. Woodcrest is the bright spot and some marginal upside in terms of revenue but nothing to write home about. A concern on margins for Q4 and the discussion on share still up in the air as Otellini claims they gained overall share and it isn't clear from a quick glance at AMD's call whether they believe they gained any. However, I'll be reviewing that in detail next and will see if we can call it. For now, Intel needs to stay the course and focus on ramping Core 2 desktop, get the right chipsets/boards into the channels and help their OEM customers get off to a quick start as they introduce products this quarter for Christmas.

I'll be reviewing AMD's results next and will be able to figure out what I think Q4 will look like based on that.

Thursday, October 19, 2006

Come back on the weekend

I'm still kind of tied up so don't have time to do an in depth analysis on Intel's earnings right now. A couple of things that caught my attention:

1. They exceeded targets slightly which was kind of in line with my overall prediction that they would be on track to hit their target. They exceeded the mid point by 100 mln $ which is ok. But the bigger take away is Intel is focussed on executing again and we will begin seeing mometum return to them in Q4.

2. Market share - Otellini is now reserving market share comments till folks like Gartner/IDC confirm in 2-3 months. I guess he learned his lesson from the Q1 fiasco not to trust his sales guys on this number. He did however say he believed they gained market share in DP server (which is the volume) with Wodcrest. Let's see if Hector provides an indication or we'll have to wait some more for this data.

3. Q4 gross margins - this was the most disappointing piece that margins would remain around 50%. This either means the price war will continue or incremental costs in the factory...possibly due to the 45nm costs kicking in. There was some discussion on this during the analysts call but I didn't have time to hear it completely.

Come back on the weekend. I'll be reviewing Intel and AMD's results in some more detail. Meanwhile, I've had to help Sharikou by correcting some basic flaws in his calculations on capacity and cash flows.

My comment on capacity can be found far down here:

http://sharikou.blogspot.com/2006/10/charlie-showed-some-wisdom.html

My comment on cash flows will show up here if the post is authorized. In all fairness, I think only one of my posts was not put up so I don't want to make it appear like all my comments are being filtered:

http://sharikou.blogspot.com/2006/10/another-look-at-intels-balance-sheet.html

Hopefully, see ya on the weekend.

1. They exceeded targets slightly which was kind of in line with my overall prediction that they would be on track to hit their target. They exceeded the mid point by 100 mln $ which is ok. But the bigger take away is Intel is focussed on executing again and we will begin seeing mometum return to them in Q4.

2. Market share - Otellini is now reserving market share comments till folks like Gartner/IDC confirm in 2-3 months. I guess he learned his lesson from the Q1 fiasco not to trust his sales guys on this number. He did however say he believed they gained market share in DP server (which is the volume) with Wodcrest. Let's see if Hector provides an indication or we'll have to wait some more for this data.

3. Q4 gross margins - this was the most disappointing piece that margins would remain around 50%. This either means the price war will continue or incremental costs in the factory...possibly due to the 45nm costs kicking in. There was some discussion on this during the analysts call but I didn't have time to hear it completely.

Come back on the weekend. I'll be reviewing Intel and AMD's results in some more detail. Meanwhile, I've had to help Sharikou by correcting some basic flaws in his calculations on capacity and cash flows.

My comment on capacity can be found far down here:

http://sharikou.blogspot.com/2006/10/charlie-showed-some-wisdom.html

My comment on cash flows will show up here if the post is authorized. In all fairness, I think only one of my posts was not put up so I don't want to make it appear like all my comments are being filtered:

http://sharikou.blogspot.com/2006/10/another-look-at-intels-balance-sheet.html

Hopefully, see ya on the weekend.

Saturday, October 14, 2006

A few days of silence

I'm going to be away and kind of busy for a few days. May not get to post but will definitely make time to come back and look at Intel's Q3 results on the 17th. I will however check in and ensure comments get through. Till then, remember my prediction:

Intel will regain market share and momentum (share + margins) in Q4. If you wanted my advice, I would have told you to buy Intel at 17$. Now, buy AMD when it goes below 22 and hold till they re-gain traction. Remember - I'm not qualified to give you this kind of advice and you are not expected to take it. But hey...it's the Internet and heaven knows what other kooky things you may have been learning on it.

Intel will regain market share and momentum (share + margins) in Q4. If you wanted my advice, I would have told you to buy Intel at 17$. Now, buy AMD when it goes below 22 and hold till they re-gain traction. Remember - I'm not qualified to give you this kind of advice and you are not expected to take it. But hey...it's the Internet and heaven knows what other kooky things you may have been learning on it.

Friday, October 13, 2006

AMD + ATI to cut 2000

The combined AMD/ATI will cut 2000 jobs:

http://www.theinquirer.net/default.aspx?article=35046

While it's sad that even two companies who seem to be on a roll will hack of 15% of their combined workforce, I think this is a smart move. It is better to remove the excess now when they can afford it. However, I wonder how the 800 AMD employees who are going to be laid off must be feeling. Undoubtedly some of them will feel they have given their blood+sweat+tears to bring AMD so far and will feel betrayed to be dropped like an old shoe. Alas, such is life.

----------------------------------------------------

UPDATE

This rumour from the Inquirer was false. The rumours have died. I've come back to update this because there are some folks who read this blog and take every comment rather personally. They've been rather insistent so I thought I'd give in. Having said that, anyone who can mis-read this post as a prediction of doom for AMD needs to get out for a bit. I mean how many ways can you mis-interpret a post where I say this is a smart move. Anyways...for some strange reason I think I'll actually be able to get on with my life even after this -:)

http://www.theinquirer.net/default.aspx?article=35046

While it's sad that even two companies who seem to be on a roll will hack of 15% of their combined workforce, I think this is a smart move. It is better to remove the excess now when they can afford it. However, I wonder how the 800 AMD employees who are going to be laid off must be feeling. Undoubtedly some of them will feel they have given their blood+sweat+tears to bring AMD so far and will feel betrayed to be dropped like an old shoe. Alas, such is life.

----------------------------------------------------

UPDATE

This rumour from the Inquirer was false. The rumours have died. I've come back to update this because there are some folks who read this blog and take every comment rather personally. They've been rather insistent so I thought I'd give in. Having said that, anyone who can mis-read this post as a prediction of doom for AMD needs to get out for a bit. I mean how many ways can you mis-interpret a post where I say this is a smart move. Anyways...for some strange reason I think I'll actually be able to get on with my life even after this -:)

Thursday, October 12, 2006

Dell sucking AMD's capacity (& life) dry

In spite of dialling down the cache from 1MB to 512kb and removing some SKUs it appears AMD is running into a capacity shortage thanks to Dell having first right of refusal on supply:

http://www.theinquirer.net/default.aspx?article=35004

I was beginning to think they had avoided this pitfall but it appears not (scroll down the comments here).

http://sharikou180.blogspot.com/2006/09/amd-won-dell-2-years-too-late-im-not.html

The implications of this are two fold:

1. Dell probably buys on shorter cycles than most other customers to keep inventory low. However, due to their size AMD and Intel probably have to keep a buffer aside for Dell in order to meet their contractual obligations. What this means is if Dell is not moving their SKUs, they still have to hold the inventory for some time thereby starving other customers when capacity is constrained.

2. The fall out of #1 above in this case for AMD is that distribution and unbranded channel without stock will be ticked off that they are losing sales to someone else and begin to put their weight behind someone who can guarantee supply. In this case Intel. The key issue is their "faith" in the supplier is lost. This is exactly why Intel lost significant market share when they had a chipset shortage. And now AMD is going to lose the trust of the channel and they will put their sales push behind Pentium & Core 2 where availability is less of an issue. In addition, they will be further ticked because Dell will be under-cutting them so now AMD is not only starving them of supply but helping the big OEM eat their breakfast.

As the shortage escalates, this becomes a proportionately bigger and longer term issue for AMD. Think about it - the small unbranded DIY guy sitting in his store, customer walks in and asks for PC - what's he going to do...push AMD when he doesn't have stock or push Intel.

The INQ article links to this post on Hexus.net:

http://www.hexus.net/content/item.php?item=6890

Which links to this apology to customers from Mesh Computers in the UK. As you can see, they don't appreciate being on the back foot and willing to push Intel instead:

http://forums.hexus.net/showthread.php?t=87080

So I had a look at the Mesh web site to see whether they had indeed increased their Intel push. The answer is yes - only 6 out of 30 desktop SKUs on offer are AMD...everything else Intel:

Mesh Computers All Desktops

So it appears winning Dell may not only be too late, it may be at an awkard time. It would have been better to win Dell once their 65nm was ramped and reducing any capacity issues. Even 2 quarters of shortage will be a problem as channel momentum will swing Intel's way and re-gaining that momentum across hundreds of thousands of channel players across the world is a BIG task that takes time.

If this capacity shortage is true, it is potentially a big issue for AMD. Specially if Dell is squeezing them on margins and then dropping systems at super low prices as it appears they are. It's a double edged sword with just one head to cut.

I repeat, AMD will lose market share in Q4 if not earlier. Momentum will swing back toward Intel with market share gain from Q4 as well as margins improving from the projected 49% in Q3.

http://www.theinquirer.net/default.aspx?article=35004

I was beginning to think they had avoided this pitfall but it appears not (scroll down the comments here).

http://sharikou180.blogspot.com/2006/09/amd-won-dell-2-years-too-late-im-not.html

The implications of this are two fold:

1. Dell probably buys on shorter cycles than most other customers to keep inventory low. However, due to their size AMD and Intel probably have to keep a buffer aside for Dell in order to meet their contractual obligations. What this means is if Dell is not moving their SKUs, they still have to hold the inventory for some time thereby starving other customers when capacity is constrained.

2. The fall out of #1 above in this case for AMD is that distribution and unbranded channel without stock will be ticked off that they are losing sales to someone else and begin to put their weight behind someone who can guarantee supply. In this case Intel. The key issue is their "faith" in the supplier is lost. This is exactly why Intel lost significant market share when they had a chipset shortage. And now AMD is going to lose the trust of the channel and they will put their sales push behind Pentium & Core 2 where availability is less of an issue. In addition, they will be further ticked because Dell will be under-cutting them so now AMD is not only starving them of supply but helping the big OEM eat their breakfast.

As the shortage escalates, this becomes a proportionately bigger and longer term issue for AMD. Think about it - the small unbranded DIY guy sitting in his store, customer walks in and asks for PC - what's he going to do...push AMD when he doesn't have stock or push Intel.

The INQ article links to this post on Hexus.net:

http://www.hexus.net/content/item.php?item=6890

Which links to this apology to customers from Mesh Computers in the UK. As you can see, they don't appreciate being on the back foot and willing to push Intel instead:

http://forums.hexus.net/showthread.php?t=87080

So I had a look at the Mesh web site to see whether they had indeed increased their Intel push. The answer is yes - only 6 out of 30 desktop SKUs on offer are AMD...everything else Intel:

Mesh Computers All Desktops

So it appears winning Dell may not only be too late, it may be at an awkard time. It would have been better to win Dell once their 65nm was ramped and reducing any capacity issues. Even 2 quarters of shortage will be a problem as channel momentum will swing Intel's way and re-gaining that momentum across hundreds of thousands of channel players across the world is a BIG task that takes time.

If this capacity shortage is true, it is potentially a big issue for AMD. Specially if Dell is squeezing them on margins and then dropping systems at super low prices as it appears they are. It's a double edged sword with just one head to cut.

I repeat, AMD will lose market share in Q4 if not earlier. Momentum will swing back toward Intel with market share gain from Q4 as well as margins improving from the projected 49% in Q3.

Thursday, October 05, 2006

Intel to buy Nvidia

Speculation that Intel will announce acquisition of Nvidia today:

Intel to take over Nvidia

My own instinct is that an acquisition is probably not the best solution if all they're after is technology. A stake in Nvidia or even a JV or a MOU type arrangement to co-develop certain technologies are better paths to gaining advantage of Nvidia's technical capabilities. However, from a business standpoint having Nvidia's comprehensive product line up and brand will be a good counter to how AMD may try to leverage the huge strength of the ATI brand. Whatever it is...any kind of alliance between Intel and Nvidia is BIG!

--------------------------------------------------------------------------------

UPDATED

The weekend is here and Intel has still not bought it's bagful of (graphic) chips. I think this deal is not a deal. But something is in the works between the two. Collaboration is inevitable. The enemy of my enemy is my friend. Neither Intel nor Nvidia will want AMD/ATI to strengthen because they are now going to feed each other. Nvidia also does not want Intel to strengthen because it is also a competitor...though the lesser of the two evils. However, with Intel's intention to get into discrete graphics, they are heading for a collision. What choices does Nvidia have - become an end to end CPU+GPU company. Easier said than done. Or find a partnership with someone else who can help them get there. As I said in a post earlier, Nvidia and Intel will get closer. I'm sure something will happen by the end of the year.

Intel to take over Nvidia

My own instinct is that an acquisition is probably not the best solution if all they're after is technology. A stake in Nvidia or even a JV or a MOU type arrangement to co-develop certain technologies are better paths to gaining advantage of Nvidia's technical capabilities. However, from a business standpoint having Nvidia's comprehensive product line up and brand will be a good counter to how AMD may try to leverage the huge strength of the ATI brand. Whatever it is...any kind of alliance between Intel and Nvidia is BIG!

--------------------------------------------------------------------------------

UPDATED

The weekend is here and Intel has still not bought it's bagful of (graphic) chips. I think this deal is not a deal. But something is in the works between the two. Collaboration is inevitable. The enemy of my enemy is my friend. Neither Intel nor Nvidia will want AMD/ATI to strengthen because they are now going to feed each other. Nvidia also does not want Intel to strengthen because it is also a competitor...though the lesser of the two evils. However, with Intel's intention to get into discrete graphics, they are heading for a collision. What choices does Nvidia have - become an end to end CPU+GPU company. Easier said than done. Or find a partnership with someone else who can help them get there. As I said in a post earlier, Nvidia and Intel will get closer. I'm sure something will happen by the end of the year.

Wednesday, October 04, 2006

The battery (non) issue

I had a few comments asking for a post on this issue of "batteries are exploding because of Intel CPUs" theory Sharikou has propogated. Here are my thoughts:

1. Do you seriously believe Sony has not closely investigated the issue to analyse root cause and would replace millions of $s of batteries thereby hammering what looked like a reasonable financial year after a long time if they could pass the blame to someone else? Do you think Sony is subservient to Dell, HP, Apple that they would take a 400+ (and counting) million $ hit. Sony is not dependant on these companies to survive unlike AMD, Intel and Microsoft. If they could save the money and more importantly their reputation for manufacturing excellence which affects their brand and hence other parts of their business, we would see a court case of humungous proportions.

2. If the issue were the thermals on Centrino and not a manufacturing glitch in the batteries, how would a battery re-call help? The risk of explosions persists by the same formula and the OEMs are waiting for the biggest consumer class action law suit ever to happen. I think not!

3. Sharikou believes he can pull off a cheap magic trick by simply saying because all batteries must be turned on to explode and all laptops have Intel CPUs consuming power...hence 1+1 = 3. Actually, the trick is if he says it often enough, with sufficient vehemence and calls you stupid then it will be true. Bottomline - there is a big fat ZERO impact to Intel from this.

4. Finally, this is a waste of time - mine and everyone else with two ounces of intelligence which is all you folks on this blog. Let's get past it and move on to topics that merit discussion. If I wanted to do a blog on things that lacked intelligence - we'd be discussing world politics.

---------------------------------------------------------------------------------------------

UPDATE

I think it's time to end this discussion once and for all. All 3 Apple notebook models affected by the re-call are G4's - not Macbook or Macbook Pro's. Hence, Sharikou's argument that the battery explosions are due to Intel CPUs is now officially dead & defunct. My advice to him - "Get over it quickly! Or your blog will lose credibility."

1. Do you seriously believe Sony has not closely investigated the issue to analyse root cause and would replace millions of $s of batteries thereby hammering what looked like a reasonable financial year after a long time if they could pass the blame to someone else? Do you think Sony is subservient to Dell, HP, Apple that they would take a 400+ (and counting) million $ hit. Sony is not dependant on these companies to survive unlike AMD, Intel and Microsoft. If they could save the money and more importantly their reputation for manufacturing excellence which affects their brand and hence other parts of their business, we would see a court case of humungous proportions.

2. If the issue were the thermals on Centrino and not a manufacturing glitch in the batteries, how would a battery re-call help? The risk of explosions persists by the same formula and the OEMs are waiting for the biggest consumer class action law suit ever to happen. I think not!

3. Sharikou believes he can pull off a cheap magic trick by simply saying because all batteries must be turned on to explode and all laptops have Intel CPUs consuming power...hence 1+1 = 3. Actually, the trick is if he says it often enough, with sufficient vehemence and calls you stupid then it will be true. Bottomline - there is a big fat ZERO impact to Intel from this.

4. Finally, this is a waste of time - mine and everyone else with two ounces of intelligence which is all you folks on this blog. Let's get past it and move on to topics that merit discussion. If I wanted to do a blog on things that lacked intelligence - we'd be discussing world politics.

---------------------------------------------------------------------------------------------

UPDATE

I think it's time to end this discussion once and for all. All 3 Apple notebook models affected by the re-call are G4's - not Macbook or Macbook Pro's. Hence, Sharikou's argument that the battery explosions are due to Intel CPUs is now officially dead & defunct. My advice to him - "Get over it quickly! Or your blog will lose credibility."

Tuesday, October 03, 2006

HP does Voodoo

Last week HP decided to buy Voodoo PC. Rahul wrote a long blog post on how it all happened and what the future could hold:

http://voodoopc.blogspot.com/2006/09/project-vampire-is-about-to-fly_28.html

While this makes sense if HP's motivation is purely to have a rebuttal or instrument to counter Dell should they get smart and begin to use the Alienware acquisition more strategically. The big question running through my head is the BIG numbers in the gaming segment are in markets like PRC and Korea. PRC will by far be the biggest market in a few years. But the Voodoo model - top of the line, super expensive niche products is not going to help them make traction in PRC. So what changes will they bring to the Voodoo brand and it's business model? Will they take it more downscale and mass market? Does that work - or does it just dilute Voodoo's equity for it's existing premium customer base?

My guess is they will do exactly that. Slot Voodoo as slightly high end brand targetted at gaming but make sure the average system price point becomes much more affordable compared to what Voodoo is today. The second thing they will do is use the brand to extend beyond PC gaming and begin to introduce other devices - not becessarily consoles but consumer electronic devices (i.e. TV's). For the die hard Voodoo fans today, this company and brand will not be the same 3 years from now.

My only other observation is Rahul seems to floating on cloud 9. His two entries on this are absolutely euphoristic. I just hope this isn't fleeting. Once they're part of the big "corporate" HP, many of their ideas and aspirations hopefully will not fall prey to corporate politics. I wish them all the best!

http://voodoopc.blogspot.com/2006/09/project-vampire-is-about-to-fly_28.html

While this makes sense if HP's motivation is purely to have a rebuttal or instrument to counter Dell should they get smart and begin to use the Alienware acquisition more strategically. The big question running through my head is the BIG numbers in the gaming segment are in markets like PRC and Korea. PRC will by far be the biggest market in a few years. But the Voodoo model - top of the line, super expensive niche products is not going to help them make traction in PRC. So what changes will they bring to the Voodoo brand and it's business model? Will they take it more downscale and mass market? Does that work - or does it just dilute Voodoo's equity for it's existing premium customer base?

My guess is they will do exactly that. Slot Voodoo as slightly high end brand targetted at gaming but make sure the average system price point becomes much more affordable compared to what Voodoo is today. The second thing they will do is use the brand to extend beyond PC gaming and begin to introduce other devices - not becessarily consoles but consumer electronic devices (i.e. TV's). For the die hard Voodoo fans today, this company and brand will not be the same 3 years from now.

My only other observation is Rahul seems to floating on cloud 9. His two entries on this are absolutely euphoristic. I just hope this isn't fleeting. Once they're part of the big "corporate" HP, many of their ideas and aspirations hopefully will not fall prey to corporate politics. I wish them all the best!

Subscribe to:

Posts (Atom)